Fill a Valid California 100X Form

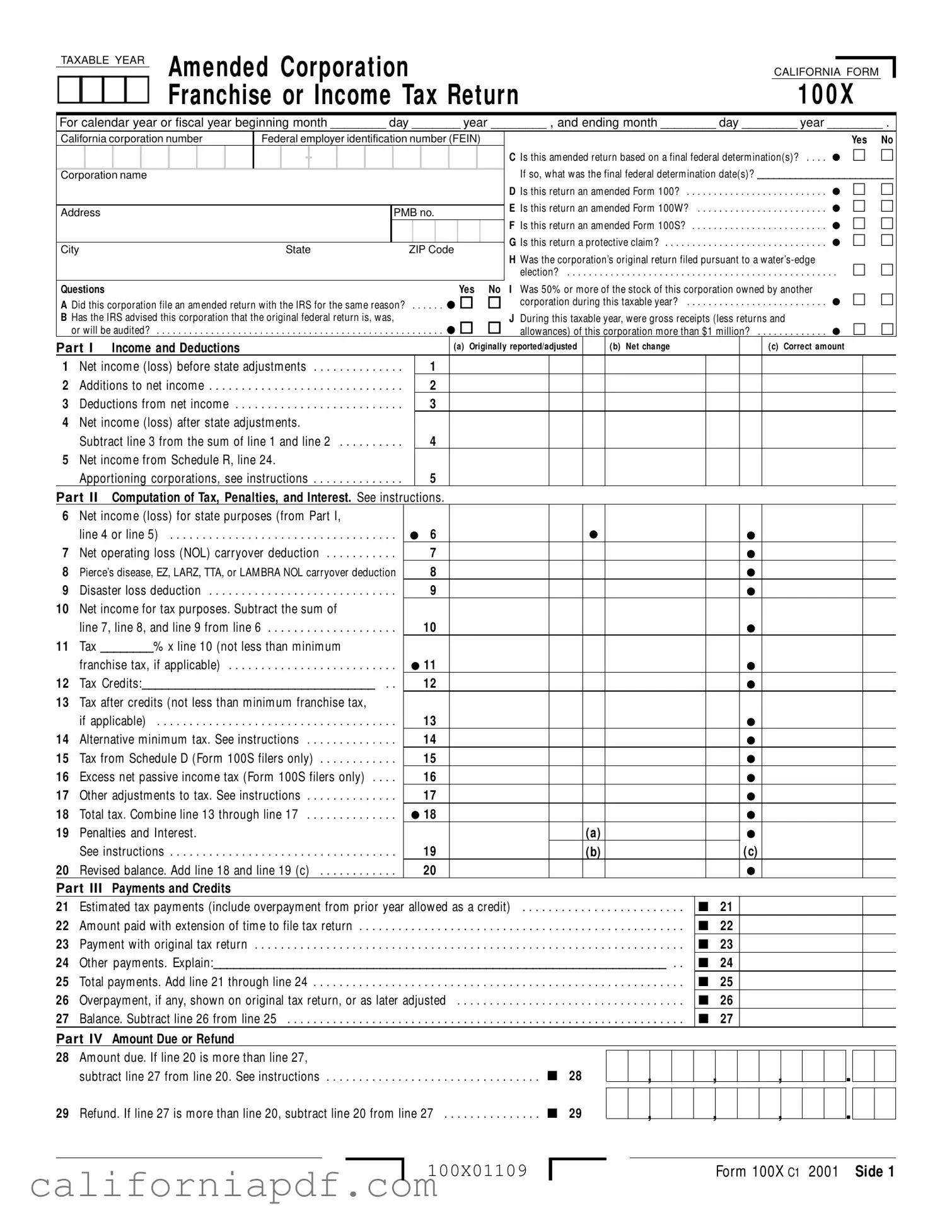

The California 100X form serves a crucial function for corporations looking to amend previously filed tax returns, either because of errors, overlooked deductions, or in response to changes following an IRS audit. This form, officially titled the Amended Corporation Franchise or Income Tax Return, is tailored for various types of filers, including C corporations, S corporations, and even financial institutions, adapting to a broad spectrum of amendments, from straightforward income adjustments to complex recalculations of tax liabilities, credits, and penalties. Crucially, the 100X form stands as the gateway for companies to correct their financial narrative with the State, ensuring their tax obligations reflect their actual fiscal status. It guides through recalculating tax dues or refunds with intricate details, such as net income modifications, tax credit reevaluations, and even addresses specific circumstances through questions aimed at uncovering the full context behind the amendment. All told, this document not only underscores the dynamic nature of corporate taxation but also underscores the importance of timely and accurate tax compliance, providing a structured framework for rectifying past tax submissions in alignment with California's tax laws.

Document Example

TAXABLE YEAR |

Amended Corporation |

CALIFORNIA |

FORM |

|

|

|

|

Franchise or Income Tax Return |

|

|

|

1 0 0 X |

|||

For calendar year or fiscal year beginning month ________ day _______ year ________ , and ending month ________ day ________ year ________ . |

|||||||||||||||||||||||||||||||||||||||

California corporation number |

|

Federal employer identification number (FEIN) |

|

|

|

|

|

|

|

|

|

|

|

Yes |

No |

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C Is this am ended return based on a final federal determ ination(s)? |

. . . . |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If so, what was the final federal determ ination date(s)? _________________________ |

|||||||||||||

Corporation name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D Is this return an am ended Form 100? . . |

. . |

. . |

. . . . |

. . . . |

. . . . . . . . |

. . . . |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

E Is this return an am ended Form 100W? |

|

|

|

|

|

|

||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

PMB no. |

|

. . |

. . |

. . . . |

. . . . |

. . . . . . . . |

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.F Is this return an am ended Form 100S? |

. . |

. . |

. . . . |

. . . . |

. . . . . . . . |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

G Is this return a protective claim ? |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . |

. . |

. . . . |

. . . . |

. . . . . . . . |

||||||||

City |

|

|

|

|

|

|

|

|

|

State |

ZIP Code |

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

H Was the corporation’s original return filed pursuant to a |

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

election? . . . |

. . . . |

. . . . . . . . . . . . . . . . . |

. . |

. . |

. . . . |

. . . . |

. . . . . . . . |

. . . . . . |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Was 50% or m ore of the stock of this corporation owned by another |

|

||||||||||||

Questions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Yes |

No I |

|

||||||||||||||||

A Did this corporation file an am ended return with the IRS for the sam e reason? |

|

. |

. |

. . |

. |

. |

corporation during this taxable year? . . |

. . |

. . |

. . . . |

. . . . |

. . . . . . . . |

. . . . |

||||||||||||||||||||||||||

B Has the IRS advised this corporation that the original federal return is, was, |

|

|

|

|

|

|

|

|

|

|

|

J During this taxable year, were gross receipts (less returns and |

|

|

|

||||||||||||||||||||||||

or will be audited? |

. . . . . . |

. . . . |

. |

. . |

. |

. |

. |

. . |

. |

. |

allowances) of this corporation m ore than $1 m illion? |

. . . . |

|||||||||||||||||||||||||||

Part I |

Income and Deductions |

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) Originally reported/adjusted |

|

( b) Net change |

|

|

|

|

(c) Correct amount |

|

||||||||||||||||

1 |

Net incom e (loss) before state adjustm ents |

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

2 |

. . . . . . . . . . .Additions to net incom e |

. . . . . |

. . . . |

. . . . |

. . . . |

. . |

|

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

3 |

. . . . . . .Deductions from net incom e |

. . . . . |

. . . . |

. . . . |

. . . . |

. . |

|

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

4 |

Net incom e (loss) after state adjustm ents. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

Subtract line 3 from the sum of line 1 and line 2 |

4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

5 |

Net incom e from Schedule R, line 24. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

Apportioning corporations, see instructions |

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

Part II |

Computation of Tax, Penalties, and Interest. See instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

6 |

Net incom e (loss) for state purposes (from Part I, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

line 4 or line 5) |

. . . . |

. . . . |

. . . . |

. |

6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

7 |

. . . . . . . . . . .Net operating loss (NOL) carryover deduction |

7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

8 |

Pierce’s disease, EZ, LARZ, TTA, or LAM BRA NOL carryover deduction |

8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

9 |

Disaster loss deduction |

. . . . |

. . . . |

. . . . |

. |

9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

10 |

Net incom e for tax purposes. Subtract the sum of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

line 7, line 8, and line 9 from line 6 |

. . |

. . . . . |

. . . . |

. . . . |

. . . . |

. |

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

11 |

Tax ________% x line 10 (not less than m inim um |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

franchise tax, if applicable) |

. . . |

. . . . . |

. . . . |

. . . . |

. . . . |

. |

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

12 |

Tax Credits:___________________________________ . . |

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

13 |

Tax after credits (not less than m inim um franchise tax, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

if applicable) |

. . . . |

. . . . |

. . . . |

. |

13 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

14 |

Alternative m inim um tax. See instructions |

14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

15 |

Tax from Schedule D (Form 100S filers only) |

15 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

16 |

Excess net passive incom e tax (Form 100S filers only) . . . . |

16 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

17 |

Other adjustm ents to tax. See instructions |

17 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

18 |

Total tax. Com bine line 13 through line 17 |

18 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

19 |

Penalties and Interest. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) |

|

|

|

|

|

|

|

|

||||||||

|

. . . . . . . . . . . . . . . . . . . . . .See instructions |

. . . . |

. . . . |

. . . . |

. |

19 |

|

|

|

|

|

|

|

|

(b) |

|

|

|

|

(c) |

|

|

|

|

|||||||||||||||

20 |

Revised balance. Add line 18 and line 19 (c) |

20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

Part III |

Payments and Credits |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

21 |

Estim ated tax paym ents (include overpaym ent from prior year allowed as a credit) |

. . . . . |

. . . . . |

. . . |

. . . . . . . . . . . . |

21 |

|

|

|

|

|

||||||||||||||||||||||||||||

22 |

Am ount paid with extension of tim e to file tax return |

|

. |

. . |

|

. . |

. |

. . . |

. |

. |

. . . |

. . |

. . . . |

. . . . . . |

. . . |

. . . . . . . . . . . . |

22 |

|

|

|

|

|

|||||||||||||||||

23 |

Paym ent with original tax return . . . . |

. . . . . |

. . . . |

. . . . |

. . . . |

. . |

. . |

|

. |

. . |

|

. . |

. |

. . . |

. |

. |

. . . |

. . |

. . . . |

. . . . . . |

. . . |

. . . . . . . . . . . . |

23 |

|

|

|

|

|

|||||||||||

24 |

Other paym ents. Explain:____________________________________________________________________ . . |

24 |

|

|

|

|

|

||||||||||||||||||||||||||||||||

25 |

Total paym ents. Add line 21 through line 24 |

. |

. . |

|

. . |

. |

. . . |

. |

. |

. . . |

. . |

. . . . |

. . . . . . |

. . . |

. . . . . . . . . . . . |

25 |

|

|

|

|

|

||||||||||||||||||

26 |

Overpaym ent, if any, shown on original tax return, or as later adjusted |

. . . . . |

. . . . . |

. . . |

. . . . . . . . . . . . |

26 |

|

|

|

|

|

||||||||||||||||||||||||||||

27 |

Balance. Subtract line 26 from line 25 |

. |

. . |

|

. . |

. |

. . . |

. |

. |

. . . |

. . |

. . . . |

. . . . . . |

. . . |

. . . . . . . . . . . . |

27 |

|

|

|

|

|

||||||||||||||||||

Part IV |

Amount Due or Refund |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

28 |

Am ount due. If line 20 is m ore than line 27, |

|

|

|

subtract line 27 from line 20. See instructions |

28 |

|

29 |

Refund. If line 27 is m ore than line 20, subtract line 20 from line 27 |

29 |

, |

, |

, |

, |

, |

, |

.

.

100X01109

Form 100X C1 2001 Side 1

Part V Explanation of Changes

1 Enter nam e, address, and California corporation num ber used on original tax return (if sam e as shown on this am ended return, write “ Sam e” ).

California corporation number |

Federal employer identification number (FEIN) |

-

Corporation name

Address |

|

PMB no. |

|

|

||

|

|

|

|

|

|

|

City |

State |

ZIP Code |

|

|

||

|

|

|

|

|

|

|

2Explanation of Changes to items in Part I, Part II, Part III, and Part IV.

Enter the line num ber from Side 1 for each item that is changing and give the reason for each change. Attach all supporting form s and schedules for item s changed. Include federal schedules if a change was m ade to the federal return. Be sure to include the corporation nam e and California corporation num ber on each attachm ent. Refer to the instructions and form s in the tax booklet for the year that is being am ended.

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________________________

|

Under penalties of perjury, I declare that I have filed an original return and I have examined this amended return, including accompanying schedules and statements, and to |

||||||||||||||||||||

Please |

the best of my knowledge and belief, this amended return is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which |

||||||||||||||||||||

Sign |

preparer has any knowledge. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Signature of officer |

|

Title |

|

Date |

|

Telephone |

|||||||||||||||

Here |

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Preparer’s signature |

|

|

Date |

|

|

Check if self- |

|

|

|

Paid preparer’s SSN/PTIN |

||||||||||

Paid |

|

|

|

|

|

employed |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FEIN |

|||||||||

Preparer’s |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Firm’s name (or yours, if |

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

|

|

|

|

|||

Use Only |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

Telephone |

|||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

( |

|

|

) |

|

|

|

|

|

|

|

||||

Where to File Form 100X

If the Form 100X results in a refund or no am ount due, m ail the am ended tax return to:

FRANCHISE TAX BOARD

PO BOX 942857

SACRAM ENTO CA 94257- 0500

If the Form 100X results in an am ount due, m ail the am ended tax return to:

FRANCHISE TAX BOARD

PO BOX 942857

SACRAM ENTO CA 94257- 0501

Side 2 Form 100X C1 2001

100X01209

For Privacy Act Notice, get form FTB 1131.

Instructions for Form 100X

Amended Corporation Franchise or Income Tax Return

General Information

Income year vs. taxable year

Effective for years beginning on or after Januar y 1, 2000, references to “ incom e year” w ere replaced w ith “ taxable year” in all provisions of the Corporation Law (CTL), the Adm inistration of the Franchise and Incom e Tax Law (AFITL), and the Personal Incom e Tax Law (PITL) . When referring to an incom e

m easurem ent period beginning before Januar y 1, 2000, the term “ taxable year” should be interpreted to m ean “ incom e year” .

Statute of limitation

California Revenue and Taxation Code Section 19306 w as am ended to provide that the statute of lim itation (SOL) for a refund w ill be four years from the later of the original due date or the date the tax return w as filed. This law change is effective for any year w ith an open SOL for issuing a refund as of Januar y 1, 2000. If the tax return is delinquent, the SOL for refund w ill revert back to four years from the original due date, not the extended due date.

Preparer Tax Identification Number (PTIN) Beginning Januar y 1, 2000, tax professionals have the option of providing their individual Social Security Num ber (SSN) or Preparer Tax Identification Num ber (PTIN) on returns they prepare. Preparers w ho w ant a PTIN m ust com plete and subm it federal Form W- 7P, Application for Preparer Tax Identification Num ber, to the IRS.

A Purpose

Use Form 100X to am end a previously filed Form 100, California Corporation Franchise or Incom e Tax Return; Form 100W, California Corporation Franchise or Incom e Tax Return – Water’s- Edge Filers; or Form 100S, California S Corporation Franchise or Incom e Tax Return.

A claim for refund of an overpaym ent of tax should be m ade by filing a Form 100X.

If the corporation is filing an am ended tax return in response to a billing notice the corporation received, the corporation w ill continue to receive billing notices until the am ended tax return is accepted. In addition, the corporation m ust pay the assessed tax before the corporation can claim a refund for any part of the assessed tax.

Note: Do not use this form to change the corporate filing status. If changing corporate status from a C corporation to an S corpora- tion, or vice versa, file form FTB 3560,

S Corporation Election or Term ination/ Revocation.

Unless other w ise stated, the term “ corpora- tion” as used in Form 100X and in these instructions includes banks, financial corporations, S corporations, exem pt

hom eow ners’ associations, political organiza- tions, lim ited liability com panies; and lim ited liability partnerships classified as corporations.

B When to File

File Form 100X only after the original tax return has been filed. Corporations m ust file a claim for refund w ithin four years from the original due date of the tax return, the date the tax return w as filed, or w ithin one year from the date the tax w as paid, w hichever is later. Tax returns filed before the due date are considered as filed on the original due date.

If the federal corporate tax return is exam ined and changed by the Internal Revenue Ser vice (IRS), report these changes to the Franchise Tax Board (FTB) w ithin six m onths of the final federal determ ination by either:

•Filing Form 100X, Am ended Corporation Incom e Tax Return; or

•Sending a letter w ith copies of the federal changes to:

CORPORATION RAR FRANCHISE TAX BOARD PO BOX 942857

SACRAM ENTO CA 94257- 0501

With either m ethod, you m ust include a copy of the final federal determ ination, all underly- ing data and schedules that explain or support the federal adjustm ents. Please note that m ost penalties assessed by the IRS also apply under California law. If penalties are included in a paym ent w ith the am ended return, see the instructions for line 19, Penalties and Interest.

C Where to File

Tax Due

If tax is due, and the corporation is not required to use electronic funds transfer (EFT), m ake check or m oney order payable to the Franchise Tax Board. Write the California corporation num ber and ‘’2001 Taxable Year Form 100X’’ on the check or m oney order.

M ail Form 100X w ith the check or m oney order to:

FRANCHISE TAX BOARD PO BOX 942857

SACRAM ENTO CA 94257- 0501

Note: If the corporation m ust pay its tax liability using EFT, all paym ents m ust be rem itted by EFT to avoid penalties. See the instructions for line 28, Am ount Due.

Refund

M ail Form 100X to:

FRANCHISE TAX BOARD PO BOX 942857

SACRAM ENTO CA 94257- 0500

Private Delivery Services

California law conform s to federal law regarding the use of certain designated private deliver y services to m eet the “ tim ely m ailing as tim ely filing/paying” rule for tax returns and paym ents. See federal Form 1120, U.S. Corporation Incom e Tax Return, for a list of designated deliver y ser vices. Private delivery ser vices cannot deliver item s to PO boxes. If using one of these ser vices to m ail any item to the FTB, DO NOT use an FTB PO box. Address the am ended tax return to:

FRANCHISE TAX BOARD

SACRAM ENTO CA 95827

Private M ailbox (PM B) Number

If the corporation leases a PM B from a private business rather than a PO box from the United States Postal Service, include the box num ber in the field labeled “ PM B no.” in the address area.

Specific Line Instructions

Questions

B and C – The corporation m ust report any changes m ade by the IRS that result in additional tax to the FTB w ithin six m onths of the date of the final federal determ ination in the follow ing instances:

•Based on a federal audit;

•Reporting a final federal determ ination; or

•The IRS asked for inform ation to establish the accuracy of specific item s on the federal return and a change w as m ade.

If the IRS changes result in a refund for California, generally the corporation m ust file a claim w ithin tw o years of the IRS final determ ination date.

Be sure to include a com plete copy of the final federal determ ination and all supporting

com putations and schedules, along w ith a schedule of the adjustm ents as applicable to the corporation’s California tax liability. For m ore inform ation, get FTB Pub. 1008, Federal Tax Adjustm ents and Your Notification Responsibilities to California.

D, E, and F – Check the appropriate box to indicate w hether this Form 100X is being filed to am end a Form 100, Form 100W, or

Form 100S.

G – Check the “ Yes” box if this Form 100X is being filed as a protective claim for refund. A protective claim is a claim for refund filed before the expiration of the statute of

lim itations for w hich a determ ination of the claim depends on the resolution of som e other disputed issues, such as pending state or federal litigation or audit.

H – Corporations are not allow ed to elect or term inate a w ater’s- edge election on an am ended return. For inform ation on how to elect or term inate a w ater’s- edge election, get the Form 100- W, Water’s- Edge Booklet.

I and J – If this am ended return is being filed to report an increase or decrease to the prepaid m inim um franchise tax, answ er question I and question J.

Columns (a), (b), and (c)

Column (a) – Enter the am ounts as show n on the original or last previously am ended tax return or, if the tax return w as adjusted or exam ined, enter the am ounts that w ere determ ined by the FTB as a result of the exam ination, w hichever occurred later.

Form 100X 2001 Page 1

Column (b) – Enter the net increase or the net decrease for each line changed. List each change on Side 2, Part V, question 2 and provide an explanation and supporting schedules for each change.

Column (c) – Add any increase in colum n (b) to the am ount in colum n (a) or subtract any decrease in colum n (b) from the am ount in colum n (a) and enter the result in colum n (c) . If there is no change, enter the am ount from colum n (a) in colum n (c) .

Part I Income and Deductions

Line 5 – Net income from Schedule R

If the corporate taxpayer apportions its business incom e to California and there is a net change in the am ount of net business incom e (loss) after state adjustm ents apportioned to the corporate taxpayer, then the corporate taxpayer m ust recom pute and attach Schedule R, Apportionm ent and Allocation of Incom e.

Part II Computation of Tax, Penalties, and Interest

For additional inform ation (such as applicable tax rates or instructions on how to determ ine net operating loss carr yover, alternative

m inim um tax (AM T), excess net passive incom e tax, etc.) refer to Form 100, Form 100W, or Form 100S instructions for the taxable year being am ended.

Line 14 – Alternative minimum tax (AM T)

Note: This applies to Form 100 or Form 100W filers only.

Enter in colum n (b) the net increase or net decrease in AM T betw een the original Schedule P (100), Alternative M inim um Tax and Credit Lim itations – Corporations, or Schedule P (100W), Alternative M inim um Tax and Credit Lim itations – Water’s- Edge Filers, and the am ended Schedule P (100) or Schedule P (100W) . Be sure to attach the am ended Schedule P (100) or

Schedule P (100W) to Form 100X.

Line 17 – Other adjustments to tax

For interest adjustm ents under the “ look- back” m ethod of com pleted long- term contracts, enter the net increase or net decrease in colum n (b) . Be sure to sign the am ended form FTB 3834, Interest Com puta- tion Under the Look- Back M ethod for

Com pleted Long- Term Contracts, and attach it to Form 100X.

Also, enter in colum n (b) the net increase or net decrease of any credit recapture, LIFO recapture, or tax on installm ent sales. For

m ore inform ation, get Form 100, Form 100W, or Form 100S, Schedule J, Add- on Taxes and Recapture of Tax Credits, for taxable years 1991 through 2001 or get Form 100 or

Form 100S instructions for taxable years 1988 through 1990.

Enter the increase or decrease to the $600 prepaym ent m inim um franchise tax for qualified new corporations per California Revenue and Taxation Code Section 23221,

effective for taxable years beginning on or after January 1, 1997, and before Januar y 1, 1999. Enter the increase or decrease to the $300 prepaym ent for taxable years beginning on or after Januar y 1, 1999, and before Januar y 1, 2000. (For corporations incorpo- rating on or after Januar y 1, 2000, there is no prepaym ent.)

Line 19 – Penalties and Interest

Line 19 (a) – In colum n (b) enter the net increase or net decrease of any penalties being reported on the am ended return.

Line 19 (b) – In colum n (b) enter the net increase or net decrease of interest being reported on the am ended return.

Line 19 (c) – In colum n (c) enter the total of line 19 colum n (a) and colum n (b) .

If the corporation does not com pute the interest due, FTB w ill figure any interest due and bill the corporation. Interest accrues on the unpaid tax from the original due date of the return to the date paid. For the applicable interest rates, get FTB Pub. 1138A, Bank and Corporation Billing Inform ation.

Part III Payments and Credits

Enter any paym ents or credits on the appropriate line.

Part IV Amount Due or Refund

Line 28 – Amount due

M ake the check or m oney order payable to the

“Franchise Tax Board” for the am ount show n on line 28. Write the California corporation num ber and taxable year on the check. Attach the check to the front of Form 100X.

Note: A corporation required to pay its taxes through EFT m ust m ake all paym ents by EFT, even if the tax due on the original tax return w as paid by check or m oney order. Indicate w hich taxable year the paym ent should be applied to w hen paying by EFT.

Line 29 – Refund

If the corporation is entitled to a refund larger than the am ount claim ed on the original tax return, line 29 w ill show the am ount of refund. The FTB w ill figure any interest due and w ill include it in the refund. If you are claim ing a refund for interest previously paid, include the interest am ount on line 19.

Part V Explanation of

Changes

Line 1

If the original tax return w as filed using a different Corporation nam e, address, and/or California corporation num ber, enter the nam e, address, and California corporation num ber used on the original tax return on this line.

Line 2

Explain in detail any changes m ade to the

am ounts listed in Side 1, colum n (a) . Include in your explanation the line num ber refer- ences for both the original and am ended tax

returns and any detailed com putations. Include a copy of the federal Form 1120X and schedules if a change w as m ade to the federal return. Include the corporation’s nam e and California corporation num ber on all attachm ents.

Where to Get Tax Forms and Publications

By Internet – You can dow nload, view, and print California bank and corporation tax form s and publications. Go to our Website at:

www. ftb. ca. gov

By phone – To order 2001 business entity tax form s call (800) 338- 0505 and follow the recorded instructions. This ser vice is available to callers w ith touchtone phones from 6 a.m . to 8 p.m ., M onday through Friday except state holidays. Please allow tw o w eeks to receive your order. If you live outside of California, please allow three w eeks to receive your order.

By mail – Write to:

TAX FORM S REQUEST UNIT FRANCHISE TAX BOARD PO BOX 307

RANCHO CORDOVA CA 95741- 0307

General Toll- Free Phone Service

Our general toll- free phone ser vice is available M onday through Friday, from 7 a.m . until

8p.m and from 8 a.m . until 5 p.m . on Saturdays.

Note: We m ay m odify these hours w ithout notice to m eet operational needs.

From w ithin the |

|

|

United States |

(800) |

852- 5711 |

From outside the |

|

|

United States |

(916) |

845- 6500 |

|

(not toll- free) |

|

Assistance for persons with disabilities The FTB com plies w ith the Am ericans w ith Disabilities Act. Persons w ith hearing or speech im pairm ents call:

From voice phone

(California Relay Ser vice) . . . . (800) 735- 2922

From TTY/TDD (Direct line to FTB

custom er service) . . . . . . . . (800) 822- 6268

For all other assistance or

special accom m odations . . (800) 852- 5711

Page 2 Form 100X 2001

Form Breakdown

| Fact Name | Description |

|---|---|

| Form Purpose | California Form 100X is used to amend a previously filed Form 100, Form 100W, or Form 100S. |

| Amendment Reasons | It serves purposes such as claiming a refund of an overpayment of tax, or adjusting the reported figures following an examination by the IRS. |

| Governing Law | The form is regulated under the California Revenue and Taxation Code Section 19306, which outlines the statute of limitations for refund claims. |

| Filing Deadlines | Claims for a refund must be filed within four years from the original due date of the return, the date the return was filed, or within one year from the tax payment date, whichever is later. |

| Submission Addresses | Where to send Form 100X depends on whether the adjustment results in a refund or an amount due, with distinct addresses for each scenario provided by the Franchise Tax Board. |

How to Write California 100X

The process of amending a corporation's franchise or income tax return in California using Form 100X necessitates careful attention to detail and accuracy. This document is specifically designed for corrections or adjustments post the original filing. Whether it results from genuine errors discovered after the initial submission or adjustments following final federal determinations, this process allows corporations to reconcile their tax liabilities accurately with the California Franchise Tax Board (FTB). Understanding how to navigate this form ensures that any necessary amendments are made correctly to reflect the corporation's true fiscal responsibilities for the given tax year.

- Identify the tax year you are amending by indicating the beginning and ending months, days, and years at the top of the form.

- Enter the California corporation number and federal employer identification number (FEIN) in the designated sections.

- If the amendment is due to a final federal determination, check "Yes" for question C and provide the final federal determination date(s).

- Fill in the corporation’s name, address (including PMB no. if applicable), city, state, and ZIP code under the relevant headings.

- Answer yes or no to questions D through J, which inquire about the nature of the amended return, including if it amends a previous Form 100, 100W, 100S, or if it's a protective claim, among others.

- In Part I (Income and Deductions), input the originally reported/adjusted amounts, net changes, and correct amounts for each item meticulously in columns (a), (b), and (c).

- In Part II (Computation of Tax, Penalties, and Interest), recalculate the necessary figures based on adjustments and complete lines 6 through 20, referring to specific instructions as needed.

- Part III (Payments and Credits) should include any payments or credits not previously reflected or inaccurately reported on the original return. Update lines 21 through 26 accordingly.

- Determine the amount due or refund in Part IV by carefully completing lines 28 and 29 with the accurate recalculated figures.

- In Part V (Explanation of Changes), start by indicating if the name, address, and California corporation number are the same or have been changed. If changed, provide the previous details.

- For line 2 in Part V, comprehensively explain the changes to items in Part I, Part II, Part III, and Part IV. Clearly mention the affected line numbers and reasons for each change, attaching all supporting documents, schedules, and, if applicable, relevant federal schedules.

- Ensure the amended return is signed and dated by an authorized officer of the corporation and, if prepared by someone other than the taxpayer, by the preparer as well.

- Mail the completed Form 100X to the appropriate address depending on whether the form results in a refund or an amount due, as specified in the instructions.

Attentiveness to each step and providing thorough explanations and accurate recalculations will aid the California Franchise Tax Board in processing the amended return efficiently. This procedure not only corrects any misreporting but also aligns the corporation’s tax records with current financial realities. It’s a crucial step in ensuring compliance and financial integrity for the tax year in question.

Listed Questions and Answers

What is the California Form 100X used for?

California Form 100X, known as the Amended Corporation Franchise or Income Tax Return, is used by corporations to make corrections or amendments to a previously filed Form 100, 100W, or 100S tax return. This includes reporting any changes in income, deductions, tax credits, or tax payments that were not accurately reported in the original tax filing. Additionally, it serves as a claim for refund of an overpayment of taxes, if applicable. Corporations may need to file this form in response to federal tax adjustments, to correct errors in the initial filing, or to claim a refund that was not previously claimed.

When should a corporation file Form 100X?

Corporations should file Form 100X only after the original tax return has been filed. The deadline to file a claim for a refund with form 100X falls within four years from the original due date of the return, the date the return was filed, or within one year from the date the tax was paid, whichever is later. Additionally, if the Internal Revenue Service (IRS) makes adjustments to a federal tax return, a corporation must report these changes to the California Franchise Tax Board (FTB) within six months of the IRS's final federal determination. This ensures compliance and allows corporations to make necessary corrections to their state tax obligations based on federal audit outcomes.

How does a corporation file Form 100X and where should it be sent?

To file Form 100X, a corporation must first ensure that all sections of the form are accurately completed, including Part V, which provides an explanation of the changes being reported. This part of the form should detail the adjustments made and include supporting documentation or schedules that validate the amendment. If the amended return results in a refund or no additional tax due, the completed form should be mailed to the Franchise Tax Board at PO BOX 942857, Sacramento, CA 94257-0500. Conversely, if the amended return shows additional tax due, it should be sent to PO BOX 942857, Sacramento, CA 94257-0501. It's crucial to include the corporation's name and California corporation number on all correspondence to ensure proper processing.

Are there any special instructions for completing the Form 100X?

Yes, when completing Form 100X, corporations should pay close attention to the specific line instructions provided within the form's guidelines. This includes accurately reporting original amounts, adjustments, and corrected amounts across various sections of the form such as Income, Deductions, and Tax Computation. It is essential to attach any amended schedules, such as Schedule R for apportioning corporations, or Schedule P for alternative minimum tax adjustments. Additionally, a detailed explanation of all changes made should be included in Part V, ensuring to reference the relevant line numbers and providing comprehensive details to support each amendment. Understanding these instructions maximizes accuracy and compliance, facilitating a smoother amendment process.

Common mistakes

Filling out the California 100X form can be a complex process, and mistakes can lead to delays or errors in amended tax return processing. Here are nine common mistakes people make when filling out this form:

Incorrect information from the original return: Not accurately transferring amounts from the original or last amended return to column (a).

Net change errors: Failing to correctly calculate the net increase or decrease for each line item changed and incorrectly reporting these in column (b).

Incorrect final amounts: Not properly adding or subtracting the adjustments in column (b) to or from the amounts in column (a) and placing the correct final amounts in column (c).

Omitting explanations for changes: Not fully explaining the reasons for the changes made to the tax return in Part V or forgetting to provide supporting documentation for the adjustments.

Not addressing federal adjustments: Failing to report changes made by the IRS within six months of receiving the final federal determination.

Incomplete schedules: Neglecting to attach required schedules such as the amended Schedule R or Schedule P (100 or 100W) when there are net changes impacting those schedules.

Inaccurate penalties and interest calculations: Incorrectly calculating or failing to report additional penalties and interest due on the amended return.

Improper reporting of payments and credits: Not correctly reporting estimated tax payments, payments made with the original return, and other payments or credits in Part III, which can result in an inaccurate calculation of the amount due or refund.

Unsigned or undated form: Forgetting to sign and date the form, thus invalidating the submission.

To avoid these mistakes, carefully review each section of the form, and consult the instructions for Form 100X. Accuracy is crucial to ensure that your amended return is processed correctly and efficiently.

Documents used along the form

When dealing with the complexities of tax submissions and amendments in California, especially for corporations, a range of forms and documents often accompany California Form 100X, the Amended Corporation Franchise or Income Tax Return. Form 100X is instrumental for corporations looking to amend a previously filed Form 100, 100W, or 100S due to corrections, updates, or the need to claim a refund. Below is a helpful list that outlines some of the most commonly used accompanying forms and documents, each briefly described to offer clarity on their purpose and application.

- Form 100: The original California Corporation Franchise or Income Tax Return. It's the base document for corporations, detailing their income, deductions, and credits for a fiscal year.

- Form 100W: California Corporation Franchise or Income Tax Return — Water’s-Edge Filers. This form is for corporations that elect the water’s-edge method of income apportionment.

- Form 100S: California S Corporation Franchise or Income Tax Return. Used by S corporations to report their income, deductions, and taxes owed to California.

- Schedule R: Apportionment and Allocation of Income. It accompanies forms when a corporation must apportion its business income among various states.

- FTB 3539: Payment Voucher for Automatic Extension for Corporations and Exempt Organizations. It's used to make a payment for a corporation that is filing an extension for its tax return.

- FTB 3567: Installment Agreement Request. Corporations that cannot pay the full amount owed with their tax return may request a payment plan using this form.

- FTB 3588: Payment Voucher for Corporations and Exempt Organizations e-filed Returns. This voucher is for payments accompanying electronically filed returns.

- FTB 3834: Interest Computation Under the Look-Back Method for Completed Long-Term Contracts. It helps corporations calculate interest due or to be refunded under specific long-term contracts.

- Form 109: California Exempt Organization Business Income Tax Return. Used by exempt organizations that have unrelated business income.

- FTB 1131: Franchise Tax Board Privacy Notice on Collection. This document outlines the reasons the FTB collects personal information, how it may be used, and the rights of individuals regarding their personal information.

Each of these documents plays a vital role in the intricate dance of tax preparation and submission, ensuring that corporations adequately meet their reporting obligations and, when necessary, correctly amend previously filed returns. Whether addressing allocation and apportionment, requesting payment plans, or ensuring compliance with specific tax regulations for entities like S corporations or exempt organizations, these forms and documents are indispensable tools in navigating the California tax landscape.

Similar forms

The California 100X form, labeled as an Amended Corporation Franchise or Income Tax Return, shares similarities with several other documents primarily utilized for correcting or updating previously submitted tax information. One notably analogous document is the IRS form 1040X, the Amended U.S. Individual Income Tax Return. Both forms serve the purpose of making adjustments to a prior tax return. Whereas the 100X amends corporation returns in California, the 1040X applies to individual federal income tax returns, allowing taxpayers to correct errors, claim overlooked deductions, or report additional income.

Similarly, the IRS form 1120X, Amended U.S. Corporation Income Tax Return, parallels the California 100X form. The 1120X allows corporations to correct previously filed Form 1120, the standard corporate income tax return at the federal level. This adjustment may involve reporting additional income, claiming missed deductions or credits, or changing the corporation's tax liability. Both the 100X and 1120X forms provide a structured approach for businesses to rectify inaccuracies or omissions in their tax obligations.

The California form 540X, Amended Individual Income Tax Return, is another document similar to the 100X, but it caters to individual state taxpayers in California. Like the 100X enables corporations to amend their income tax returns, the 540X allows individuals to make corrections to their state income tax returns. Both forms facilitate adjustments to previously reported tax details, ensuring taxpayers can update their filings as necessary to reflect their accurate tax responsibilities.

Moreover, the IRS Form 1065X, Amended Return or Administrative Adjustment Request (AAR), has a similar function to the 100X but for partnership tax filings. Partnerships use this form to correct errors on a previously filed Form 1065 or to make certain elections after the prescribed deadline. While the 100X targets corporate entities within California, the 1065X accomplishes a similar goal for partnerships at the federal level, reinforcing the importance of accuracy and completeness in tax reporting across different entity types.

In addition, the IRS Form 941-X, Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund, compares to the 100X but in the context of employer payroll taxes. Employers utilize the 941-X to correct errors on a previously filed Form 941, such as overreported or underreported wages, tips, and taxes. Both the 941-X and the 100X address the necessity for rectifying previously submitted tax information, albeit for different taxes and with different focuses.

Analogous to state-level adjustments, the California Form 590X, Amendment to Withholding Exemption Certificate, allows for adjustments to be made regarding withholding exemptions on income sourced from California. Though pertaining to withholding rather than direct income taxation like the 100X, both documents underscore the importance of accurate tax practices and the ability to amend previously made declarations.

The S Corporation Amended Franchise or Income Tax Return in California also embodies principles similar to the 100X, adjusted for S corporations. This specificity allows S corporations, which have their own set of tax conditions and benefits, to correct or update their state tax filings. It parallels the 100X's role for C corporations, providing a state-level mechanism for tax amendments tailored to different corporate structures.

Finally, the Individual Amended Return for Nonresidents or Part-Year Residents, akin to the California 100X, facilitates amended filings for individuals not fully subject to California tax laws throughout the tax year. While aimed at individuals, the underlying premise aligns with the 100X's objective: ensuring tax filings accurately represent the taxpayer's obligations and entitlements within the specific tax period.

Through these examples, one can appreciate the universal necessity across various tax forms, including the California 100X, for providing mechanisms to correct or update previously filed tax information. These documents ensure compliance and fairness in the tax system, allowing taxpayers—be they individuals, corporations, partnerships, or employers—to rectify inaccuracies and uphold their responsibilities under the law.

Dos and Don'ts

Do:

- Ensure the corporation name, address, and all identifying numbers match the original return unless changes are necessary.

- Clearly explain the reason for each change in Part V, including line numbers for the original and amended returns as well as detailed computations.

- Attach all supporting forms, schedules, and, if applicable, federal schedules for items that have changed.

- File within the appropriate deadlines to ensure adherence to statute of limitations for refund claims.

Don't:

- Attempt to change the corporate filing status with this form. For status changes, other forms such as FTB 3560 should be used.

- Forget to sign the return. An unsigned return can delay processing and potentially result in penalties.

- Overlook entering the correct amounts in columns (a), (b), and (c) in Part I to Part IV for accurate processing.

- Ignore the need to report IRS changes to the FTB within six months of the final federal determination.

Misconceptions

One common misconception is that the California 100X form is only for businesses that owe additional taxes. This is not accurate; businesses use the form to amend previously filed tax returns whether it results in owing more taxes, requesting a refund, or reporting information correctly.

Many believe that the 100X form can be filed at any time. However, there are specific deadlines for when it must be filed, generally within four years from the original filing date or within one year from the date of the last payment.

Another misconception is that amendments can only be made if the IRS adjusts a federal return. While IRS adjustments are a common reason for amendments, businesses can file a 100X for other reasons, such as correcting errors or claiming missed deductions or credits.

Some think that amending a return using Form 100X automatically triggers an audit. Amending a return does not inherently increase the audit risk, although the information provided in the amendment is subject to review.

There's a false belief that electronic filing is not available for Form 100X. While paper filing was the norm, California has made strides toward accepting electronic submissions for many tax forms, including amendments.

Another misconception is that a 100X form amendment will process quickly, similar to an original tax return. Amendments often require manual review, which means processing times can be significantly longer.

Some business owners mistakenly believe they can change their corporation's filing status (like from C corporation to S corporation) using the 100X form. Changes in status require different forms and procedures.

It's also mistakenly believed that if you're amending a return to claim a refund, you don't need to document or explain the changes thoroughly. The FTB requires a detailed explanation of all amendments, including supporting documentation.

Lastly, there is a misconception that penalties and interest calculated for underpayments on the original return cannot be adjusted with a 100X filing. If an amendment alters the tax liability, it may also affect the assessment of penalties and interest.

Key takeaways

Filing California Form 100X is necessary to amend a previously filed Form 100, 100W, or 100S to correct financials, adjust income or deductions, or update any other information. This action might be taken to claim a refund or report additional taxes due following internal reviews or after an audit by the Internal Revenue Service (IRS).

It is critical to note that a corporation must report any federal changes to the California Franchise Tax Board (FTB) within six months of the IRS's final determination. This includes adjustments to the federal return that could affect the state tax liability. Corporations should include a complete copy of the IRS's final determination along with the amended California return to ensure a thorough review and proper adjustments by the FTB.

The statute of limitations for filing a claim for refund with the California Franchise Tax Board extends to four years from the original due date of the return or the date it was filed, whichever is later. This timeframe is crucial for corporations seeking to amend their returns, especially when aiming to claim a refund for overpaid taxes.

When completing Form 100X, it is essential to provide a detailed explanation of the changes being made. Including supporting documentation, schedules, and, if applicable, federal adjustments is necessary for the FTB to accurately process the amended return. This may involve recalculating taxes, credits, deductions, and penalties based on the amendments to the originally filed tax return.

Different PDF Templates

Form 540 Instructions 2023 - Maximize your medical and dental expense deductions with specific adjustments allowed by California, detailed in Schedule CA (540), Part II.

What Is a Dismissal Order - Designed for individuals who have fulfilled the conditions of their release and maintained a clean record thereafter.

Consumer Affairs California - The GSR-1 form is not just an application; it represents a station’s pledge to maintain high standards in emissions control and vehicle inspection, contributing to cleaner air in California.