Fill a Valid California 3500 Form

The California 3500 form is an essential document for organizations seeking tax exemption status within the state of California. Tailored to provide detailed information about an organization, from basic identifiers like corporation numbers and contact information to in-depth queries about the structure, financial data, and planned activities, this form is comprehensive in nature. It demands accurate organization information including names, addresses, and the FEIN to ensure a clear identification process. Furthermore, the form explores the organizational structure by inquiring about the type of entity applying—be it a foreign corporation, a trust, or a limited liability company. The significance of the form is heightened by its requirement for narrative descriptions of past, current, and planned activities, aiming to underscore how these activities align with the organization's tax-exempt purposes. Financial transparency is another crucial aspect, as the form requests submissions of past returns and detailed income and expense statements. Additional details such as information on officers, directors, and trustees underline the governance of the organization—ensuring there's a record of who is responsible for managing the entity. Ultimately, the meticulous completion and submission of this form to the Exempt Organizations Unit at the Franchise Tax Board play a pivotal role in the journey toward obtaining tax-exempt status in California, making it a key step for eligible organizations.

Document Example

|

|

|

|

|

|

|

|

CALIFORNIA FORM |

|

|

|

|

|

|

|

|

|||

Exemption Application |

|

|

|

|

3500 |

|

|||

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

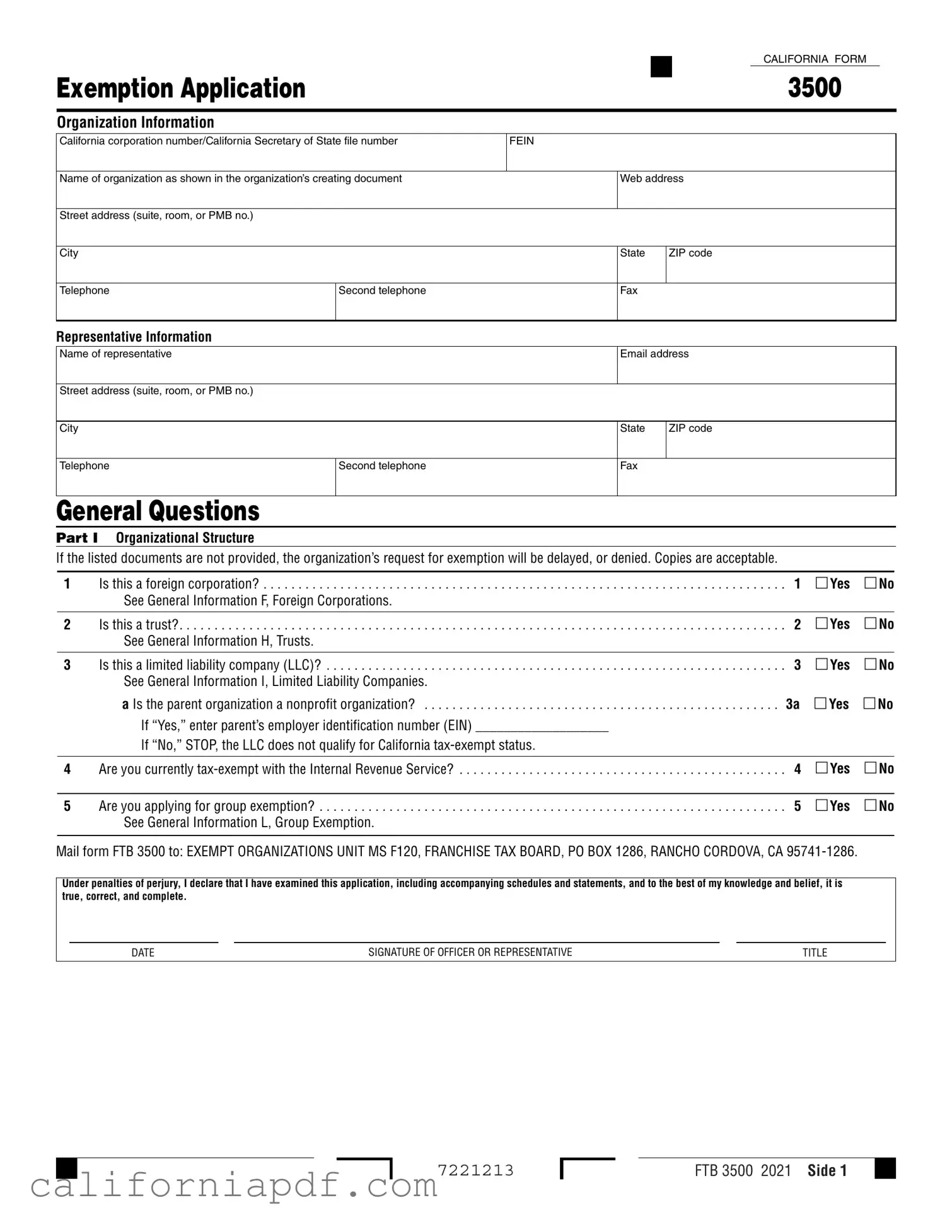

Organization Information |

|

|

|

|

|

|

|

||

California corporation number/California Secretary of State file number |

FEIN |

|

|

|

|

|

|||

|

|

|

|

|

|||||

Name of organization as shown in the organization’s creating document |

|

Web address |

|||||||

|

|

|

|

|

|

|

|

|

|

Street address (suite, room, or PMB no.) |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|||

City |

|

|

|

State |

|

ZIP code |

|||

|

|

|

|

|

|

|

|

|

|

Telephone |

|

Second telephone |

|

Fax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Representative Information |

|

|

|

|

|

|

|

||

Name of representative |

|

Email address |

|||||||

|

|

|

|

|

|

|

|

||

Street address (suite, room, or PMB no.) |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|||

City |

|

|

|

State |

|

ZIP code |

|||

|

|

|

|

|

|

|

|

|

|

Telephone |

|

Second telephone |

|

Fax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

General Questions |

|

|

|

|

|

|

|

||

Part I |

Organizational Structure |

|

|

|

|

|

|

|

|

If the listed documents are not provided, the organization’s request for exemption will be delayed, or denied . Copies are acceptable .

1 |

.Is this a foreign corporation? |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

.□. .Yes. . 1 |

□No |

|

|

See General Information F, Foreign Corporations . |

|

|

|

|

2 |

Is this a trust? |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 |

□Yes |

□No |

|

|

See General Information H, Trusts . |

|

|

|

|

3 |

Is this a limited liability company (LLC)? |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

.□. Yes. . . |

□. .No |

|

|

See General Information I, Limited Liability Companies . |

|

|

|

|

a Is the parent organization a nonprofit organization? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . □. .Yes. . .□. No. . . . . . .

If “Yes,” enter parent’s employer identification number (EIN) ___________________

If “No,” STOP, the LLC does not qualify for California

4 Are you currently

5 Are you applying for group exemption? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . □. . Yes. . . . □. 5No See General Information L, Group Exemption .

Mail form FTB 3500 to: EXEMPT ORGANIZATIONS UNIT MS F120, FRANCHISE TAX BOARD, PO BOX 1286, RANCHO CORDOVA, CA

Under penalties of perjury, I declare that I have examined this application, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete.

DATE |

SIGNATURE OF OFFICER OR REPRESENTATIVE |

TITLE |

7221213

FTB 3500 2021 Side 1

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Organization name: __________________________ |

Corp number/CA SOS file number: |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part II Narrative of Activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

1 |

Was the organization’s California |

. . . . . . . . . . . . . . . . . . . . . |

. . . . . . . |

. . □. Yes. . |

. |

.□. No. . . . . 1 |

||||||||||

|

If “No,” the organization may qualify to file form FTB 3500A, Submission of Exemption Request . For more information, get form FTB 3500A . |

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

2 |

Enter the California Revenue and Taxation Code (R&TC) section that best fits the organization’s purpose/activity |

|

|

|

|

|

|

|

|

|

|

|

||||

|

See the Exempt Classification Chart on page 6 |

. . . . . . . . . . . . . . . . . . . . . |

. . R&TC. . . . Section. . . . 23701. . . . |

. . 2 |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

3 |

Enter the date the organization formed |

. . . . . . . . . . . . . . . . . . . . . |

. . . . . ./ . |

. . |

. / . . |

. . . . . . 3 |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

mm / |

dd |

/ |

|

yyyy |

|||||

4What is the organization’s annual accounting period ending?

(must end on the last day of the calendar or fiscal year) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4 . . . . . / . . . . . . . . .

mm / dd

5What is the primary purpose of the organization?

|

|

|

|

|

|

|

6 |

Is the organization currently conducting, or plan to conduct activities? |

. 6. . |

□. .Yes. . . □. No |

|||

|

If “Yes,” enter the date the activities began, or will begin . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . /. |

. . |

. ./ |

|||

|

mm / |

dd |

|

/ |

yyyy |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Side 2 FTB 3500 2021

7222213

|

|

|

|

Organization name: __________________________ |

Corp number/CA SOS file number: |

||

Part II Narrative of Activities (continued)

7Describe the organization’s past, present, and planned activities below. Do not merely refer to or repeat the language in the organizational document . List each activity separately, in the order of importance based on the relative time and other resources devoted to the activity. Indicate the percentage of time for each activity. Each description should include a:

a Detailed description of the activity, including its purpose and how it furthers the organization’s exempt purpose . b Detailed description of when the activity was or will be initiated .

c Detailed description of where and by whom the activity will be conducted .

7223213

FTB 3500 2021 Side 3

|

|

|

|

Organization name: __________________________ |

Corp number/CA SOS file number: |

||

Part III Financial Data

1a Has the organization filed the Form 199, California Exempt Organization Annual Information Return, for the current

and prior years? |

1a □Yes |

□No |

b Has the organization filed the FTB 199N, California |

. . . □1bYes |

□No |

We will review information reported on previously filed Form 199 to determine exemption eligibility. If the FTB 199Ns were filed or no returns were filed, attach a detailed income and expense statement for the current year and three previous years . If you are not yet active, attach a proposed budget covering the next four years .

Part IV Officers, Directors, and Trustees

1List names, titles, and mailing addresses of all officers, directors, and trustees whether or not compensation is or will be paid . For each person listed, state their total annual compensation, or proposed compensation, for all services to the organization, whether as an officer, employee, or other position . Use actual figures, if available . Enter “none” if no compensation is or will be paid . If additional space is needed, attach a separate sheet .

Name

Title

Mailing Address

Compensation Amount (annual actual or estimated)

2Will any incorporator, founder, board member or other person(s) or entity:

|

a Share any facilities with the organization? |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. a. |

. □. Yes. . |

. .□. No |

|||||||

|

b Rent, sell, or transfer property to this organization? |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

b |

□Yes |

□No |

|||||||

|

c Be compensated for services other than performing as a board member or employee? |

. |

c |

□Yes |

□No |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Part V |

History |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . . . . |

||||||||

1 Has the organization been issued any previous California ID number? |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. .□. Yes. . |

. □. .No. |

|||||||||

|

|

|

|

|

|

|

|

|

||||

2 |

Was this organization’s exemption previously revoked by the Internal Revenue Service? |

. □. .Yes. . |

. □. No. . 2 |

|||||||||

|

If “Yes,” enter date revoked |

|||||||||||

|

|

|

|

mm |

/ |

|

dd |

/ |

|

yyyy |

|

|

Part VI |

Fund Raising |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

1 |

Does or will the organization participate in |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . |

. |

. |

. .□. .Yes. □. 1No. . |

||||||

|

If “Yes,” check all the |

|

|

|

|

|

|

|

|

|||

|

□ Mail solicitations |

□ Phone solicitations |

|

|

|

|

|

|

|

|

||

|

□ Email solicitations |

□ Accept donations on the organization’s website |

|

|

|

|

|

|

|

|

||

|

□ Personal solicitations |

□ Receive donations from another organization’s website |

|

|

|

|

|

|||||

|

□ Vehicle, boat, plane, or similar donations |

□ Government grant solicitations |

|

|

|

|

|

|

|

|

||

|

□ Foundation grant solicitations |

□ Other - Attach description |

|

|

|

|

|

|

|

|

||

Side 4 FTB 3500 2021

7224213

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Organization name: __________________________ |

Corp number/CA SOS file number: |

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part VII Specific Activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1 |

Does the organization conduct any gaming activities (bingo, raffles, etc .) . |

. . . . . . . . . . . . . . . . . . . . . . . |

. . . |

. . . . . . . . . |

. |

. . |

. |

. . |

. |

|

1 □Yes □No |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

Does the organization lease property from others? |

. . . . . . . . . . . . . . . . . . |

. . |

. . . . . |

. . . |

. |

. |

. |

. |

. . |

|

. . .□. Yes. . . . |

□. . No. 2 |

||

|

If “Yes,” attach copy of lease agreement . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Does the organization lease property to others? |

. . . . . . . . . . . . . . . . . . . . . . . |

. |

. |

. |

. |

. |

. |

. . □. Yes. . . |

.□. No |

|||||

|

If “Yes,” attach copy of lease agreement . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

Does or will the organization publish, sell, or distribute any literature? . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . |

. . . . . . |

. . . |

. |

. . |

. |

. . |

. |

. |

4 □Yes |

□No |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

Does or will the organization own, or have rights in music, literature, tapes, artworks, choreography, scientific discoveries, |

|

|

|

|

|

|

. . □. Yes. . . |

.□. No |

||||||

|

or other intellectual property? |

. . . . . . . . . . . . . . . . . . . . . . . |

. |

. |

. |

. |

. |

. |

|||||||

6Does or will the organization accept contributions of real property, conservation easements, closely held securities, intellectual

property such as patents, trademarks, and copyrights, works of music or art licenses, royalties, automobiles, boats, planes, or

other vehicles, or collectibles of any type? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . □. Yes. . . .□. No. . . . . . .

7Does or will the organization operate outside of the United States? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .□. Yes. . . □. .No. . . . . . .

7225213

FTB 3500 2021 Side 5

Organization name: __________________________ |

Corp number/CA SOS file number: |

Schedule 1

Section A R&TC Section 23701a – Labor, agricultural, or horticultural organization

1 Are any services to be performed for members? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1. . .□. Yes. . . . □. . No If “Yes,” explain .

2 |

Is the organization formed as a cooperative? |

|

|

If “Yes,” provide a copy of the federal exemption letter showing exemption under IRC Section 501(c)(5) |

2 □Yes □No |

Section B R&TC Section 23701b – Fraternal societies, orders, or associations, etc. (Lodge system with benefits)

Operating under the lodge system means carrying on activities under a form of organization that comprises local branches called lodges, chapters, or the like, that are largely

1 Is the organization a college fraternity or sorority or a chapter of a college fraternity or sorority? . . . . . . . . . . . . . . . . . . . . . . . 1 □Yes □No

If “Yes,” college fraternities and sororities generally qualify as organizations described in R&TC Section 23701g .

For more information, get FTB Pub 1077, Guidelines for Social and Recreational Organizations . If R&TC Section 23701g appears to apply, do not complete Section B . Go to Section G on Schedule 3, Social and recreational organization .

2Does the organization operate, or plan to operate under the lodge system or for the exclusive benefit of the members of

|

the lodge system? |

. . . . . 2 |

□Yes |

□No |

|

|

|

|

|

|

|

3 |

Is the organization a subordinate of a national or state level organization? |

. . . . 3. |

. □. .Yes. . |

. □. No |

|

|

If “Yes,” attach a certificate signed by the secretary of the parent organization certifying that the subordinate is a duly |

|

|

|

|

|

constituted body operating under the jurisdiction of the parent body. |

|

|

|

|

|

|

|

|

|

|

4 |

Is the organization a parent or grand lodge? |

. . . . . 4 |

□Yes |

□No |

|

|

|

|

|

|

|

5Describe the types of benefits (life, sick, accident, or other benefits) paid, or to be paid, to members .

Section L R&TC Section 23701l – Fraternal beneficiary societies, orders, or associations, etc. (Lodge system with no benefits)

Operating under the lodge system means carrying on activities under a form of organization that comprises local branches (called lodges, chapters, or the like) that are largely

1 Is the organization a college fraternity or sorority, or a chapter of a college fraternity or sorority? . . . . . . . . . . . . . . . 1. . □. .Yes. . . □No

If “Yes,” college fraternities and sororities generally qualify as organizations described in R&TC Section 23701g .

For more information, get FTB Pub 1077, Guidelines for Social and Recreational Organizations . If R&TC Section 23701g appears to apply, do not complete Section L . Go to Section G on Schedule 3, Social and recreational organization .

2Does the organization operate or plan to operate under the lodge system or for the exclusive benefit of the members of

|

a lodge system? |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2. . |

.□. .Yes. . . |

□No |

|

|

|

|

|

|

|

3 |

Is the organization a subordinate of a national or state level organization? |

. . . . . . . . . . . . . . . . . . . . . . . . . . . 3. |

. □. .Yes. . . □. No |

||

|

|

|

|

|

|

4 |

Is the organization a parent or grand lodge? |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 |

□Yes |

□No |

|

Side 6 FTB 3500 2021

7226213

|

|

|

|

Organization name: __________________________ |

Corp number/CA SOS file number: |

||

Schedule 2

Section D R&TC Section 23701d – Religious, charitable, scientific, literary, or educational organization

1Check the box(es) below that best describes the organization .

□ Charitable |

□ Educational |

□ Credit Counseling |

□ Synagogue |

□ School |

□ Testing for public safety |

□ Church |

□ Literary |

□ Hospital, Medical Center |

□ Temple |

□ Scientific |

□ Qualified sports organization |

□ Mosque |

□ Religious |

□ Prevent cruelty to children or animals |

2Has the organization received or expect to receive 10% or more of its assets from any organization or group of affiliated organizations (affiliated through stockholding, common ownership, or otherwise), any individuals, or members of a family

|

group (brother or sister whether whole or half blood, spouse/RDP, ancestor or lineal descendant)? |

2 |

□Yes |

□No |

|

|

|

|

|

3 |

Does the organization attempt to influence legislation? |

3. . . |

□. Yes. . . . |

□. . No |

4Does the organization support or oppose candidates in political campaigns in any way? . . . . . . . . . . . . . . . . . . . . 4. . □. Yes. . . .□. No.

5Does the organization hold, or plan to hold, 10% or more of any class of stock or 10% or more of the total combined

|

voting power of stock in any corporation? |

. 5. . |

.□. .Yes. |

□No |

|

|

|

|

|

|

|

6 |

a |

Does the organization operate as a church, mosque, synagogue, or temple? |

.6a. . |

.□. .Yes |

□No |

|

|

If “Yes,” complete Schedule 2A, Churches . |

|

|

|

|

b |

Is the organization’s main function to provide hospital or medical care? |

6b |

□Yes |

□No |

|

|

If “Yes,” complete Schedule 2B, Hospitals . |

|

|

|

|

c |

Is the organization a credit counseling organization? |

6c |

□Yes |

□No |

|

|

If “Yes,” complete Schedule 2C, Credit Counseling Organizations . |

|

|

|

7227213

FTB 3500 2021 Side 7

Organization name: __________________________ |

Corp number/CA SOS file number: |

Schedule 2A – Churches

Complete Schedule 2A only if the organization answered “Yes” to Specific Section D, Question 6a .

1Check the box that best describes the organization .

|

□Church □Mosque □Synagogue |

□Temple |

|

2 |

Has a place of worship been established? |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . □. Yes. . . .□. No |

|

|

If “Yes,” at what address? Who is the legal owner of the property? Other property use? |

||

|

If “No,” explain where religious services are held . |

||

|

|

|

|

|

|

|

|

|

|

|

|

3 Does the organization have a regular congregation or conduct religious services on a regular basis?. . . . . . . . . . . . . . . . . . . . 3 □Yes □No If “Yes,” how many usually attend the regular worship services? How often are religious services held?

If “No,” explain .

4Explain the background and training of the religious leaders .

5Will income be received from incorporators, ministers, officers, directors, or their families? . . . . . . . . . . . . . . . . . . . . □. Yes. . . .□. No5 If “Yes,” explain, including dollar amounts received .

|

|

|

6 |

Will any founder, member, or officer take a vow of poverty? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .□. Yes. . . □. .No |

|

|

If “Yes,” explain . |

|

|

|

|

|

|

|

|

|

|

7Will any founder, member, or officer transfer personal assets to this organization, like a home, automobile, furnishings,

business, or recreational assets, etc ., that will be made available for the personal use of the donors? . . . . . . . . . . . . . . . □. .Yes. . 7□No If “Yes,” explain .

Side 8 FTB 3500 2021

Schedule 2A Churches continued

7228213

|

|

|

|

Organization name: __________________________ |

Corp number/CA SOS file number: |

||

Schedule 2A – Churches (continued)

8Will any founder, member, or officer assign or donate income to the organization that will be used to pay their own personal salary, living allowance, or that will result in any other personal benefit (such as food, medical expenses, clothing,

|

insurance, etc .)? |

8 □Yes □No |

|

If “Yes,” explain . |

|

|

|

|

|

|

|

|

|

|

9 |

Does the organization have a written creed, statement of faith, or summary of beliefs? |

9 □Yes □No |

|

If “Yes,” explain . |

|

|

|

|

|

|

|

|

|

|

10 |

Do the religious leaders conduct baptisms, weddings, funerals, etc .? |

10. . . .□Yes □No |

|

If “Yes,” explain . |

|

|

|

|

|

|

|

|

|

|

11 |

Does the organization ordain, commission, or license ministers or religious leaders? |

11 □Yes □No |

|

If “Yes,” describe . |

|

|

|

|

|

|

|

7229213

FTB 3500 2021 Side 9

Organization name: __________________________ |

Corp number/CA SOS file number: |

Schedule 2B – Hospitals

Complete Schedule 2B only if the organization answered “Yes” to Specific Section D, Question 6b . Attach a statement to explain any answers .

1 |

Are all the doctors in the community eligible for staff privileges? |

1 □Yes □No |

|

If “No,” give the reasons why and explain how the medical staff is selected . |

|

2a Does or will the organization provide medical services to all individuals in the community who can pay for themselves

or have private health insurance? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2a. . . □. Yes. . . □. .No. . . . . . .

If “No,” explain .

bDoes or will the organization provide medical services to all individuals in the community who participate in

Medicare? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . □. Yes. . . .□. No. . . . . . .

If “No,” explain .

3a Does or will the organization require persons covered by Medicare or Medicaid to pay a deposit before receiving

|

|

services? |

3a |

□Yes |

□No |

|

|

If “Yes,” explain . |

|

|

|

|

b Does the same deposit requirement, if any, apply to all other patients? |

3b |

□Yes |

□No |

|

|

|

If “No,” explain . |

|

|

|

4 |

a |

Does or will the organization maintain a |

4a |

□Yes |

□No |

|

|

If “No,” explain why the organization does not maintain a |

|

|

|

|

|

services provided . |

|

|

|

|

b |

Does the organization have a policy on providing emergency services to persons without apparent means to pay? . . . . |

4b. . |

□Yes |

□No |

|

|

If “Yes,” provide a copy of the policy. |

|

|

|

cDoes the organization have any arrangements with police, fire, and voluntary ambulance services for the delivery

|

|

or admission of emergency cases? |

. . . |

.□. Yes. . 4c □No |

|

|

|

If “Yes,” describe the arrangements, including whether they are written or oral agreements . If written, submit copies of |

|

|

|

|

|

all such agreements . |

|

|

|

5 |

a |

Does the organization provide for a portion of the organization’s services and facilities to be used for charity patients? . . . |

5a |

□Yes |

□No |

|

|

If “Yes,” answer question 5b through question 5e . |

|

|

|

|

b |

Explain the organization’s policy regarding charity cases, including how the organization distinguishes between charity |

|

|

|

|

|

care and bad debts . Submit a copy of the written policy. |

|

|

|

|

c |

Provide data on the organization’s past experience in admitting charity patients, including the amounts expended for |

|

|

|

|

|

treating charity care patients and types of services provided to charity care patients . |

|

|

|

|

d |

Describe any arrangements with federal, state, or local governments or government agencies for paying for the cost |

|

|

|

|

|

of treating charity care patients . Submit copies of any written agreements . |

|

|

|

|

e |

Does the organization provide services on a sliding fee schedule depending on financial ability to pay? |

5e |

□Yes |

□No |

|

|

If “Yes,” submit the sliding fee schedule . |

|

|

|

6 |

a |

Does or will the organization carry on a formal program of medical training or medical research? |

6a |

□Yes |

□No |

|

|

If “Yes,” describe such programs, including the type of programs offered, the scope of such programs, and affiliations |

|

|

|

|

|

with other hospitals or medical care providers with which the organization carries on the medical training or research |

|

|

|

|

|

programs . |

|

|

|

|

b |

Does or will the organization carry on a formal program of community education? |

. . . |

.□. Yes6b |

□No |

|

|

If “Yes,” describe such programs, including the type of programs offered, the scope of such programs, and affiliations |

|

|

|

|

|

with other hospitals or medical care providers with which the organization offers community education programs . |

|

|

|

Schedule 2B Hospitals continued

Side 10 FTB 3500 2021

7229213

Form Breakdown

| Fact Name | Fact Detail |

|---|---|

| Form Purpose | Exemption Application for organizations |

| Governing Law | California Revenue and Taxation Code (R&TC) |

| Submission Address | EXEMPT ORGANIZATIONS UNIT MS F120, FRANCHISE TAX BOARD, PO BOX 1286, RANCHO CORDOVA, CA 95741-1286 |

| Foreign Corporation Inquiry | Question regarding the status as a foreign corporation |

| Organizational Structure Information Required | Includes questions on structure such as trusts, LLC, and Nonprofit status |

| Tax-Exempt Status with IRS | Inquiry on current tax-exempt status with the Internal Revenue Service |

| Financial Information | Questions regarding filing of Form 199 or FTB 199N and financial statements |

| Officers, Directors, and Trustees | Requirement to list names, titles, and compensation details |

| Specific Activities | Queries on gaming, leasing, publishing activities, and more |

How to Write California 3500

Completing the California Form 3500 is crucial for organizations seeking certain exemptions. This form is detailed, requiring careful attention to accurately reflect your organization's status and activities. Below are step-by-step instructions to help ensure you fill out the form correctly and completely.

- Start with the Organization Information section. Enter your California corporation number or Secretary of State file number, FEIN, and the name of your organization as it appears in founding documents. Also, provide your web address, street address, city, state, ZIP code, telephone numbers, and fax.

- In the Representative Information section, input the name, email, street address (including suite, room, or PMB no.), city, state, ZIP code, telephone numbers, and fax of a representative of your organization.

- For Part I: Organizational Structure, answer questions about whether your organization is a foreign corporation, a trust, or a limited liability company (LLC). Include any relevant explanations as required.

- Part II: Narrative of Activities asks about your organization's tax-exempt status, whether it is applying for group exemption, and if its California tax-exempt status was previously revoked. Answer each question, and enter the related information, such as the R&TC section for your organization's purpose/activity, the date your organization formed, and describe your organization’s past, present, and planned activities in detail.

- In Part III: Financial Data, disclose if the organization has filed Form 199 or the FTB 199N for the current and prior years. Attach a detailed income and expense statement for the current year and three previous years or a proposed budget for the next four years if not yet active.

- Part IV: Officers, Directors, and Trustees requires you to list names, titles, and addresses for all officers, directors, and trustees. State their total annual compensation, or proposed compensation, for their services to the organization.

- Answer questions regarding fund-raising, specific activities, and whether the organization operates outside of the United States in Part V: History, Part VI: Fund Raising, and Part VII: Specific Activities.

- Finally, sign and date the form under the penalty of perjury declaration, indicating that, to the best of your knowledge, all provided information is true, correct, and complete. Mail the completed form to the Exempt Organizations Unit address provided on the form.

Completing this form comprehensively and accurately is key to ensuring your organization's exemption application is processed without delay. Take time to review each section carefully and provide complete and detailed responses to support your request.

Listed Questions and Answers

What is the California 3500 Form?

The California 3500 Form, known as the Exemption Application, is a document organizations fill out to apply for tax-exempt status from the California Franchise Tax Board. This form requires detailed information about the organization's structure, activities, financial data, officers, directors, trustees, and any specific activities the organization may engage in.

Who needs to file the California 3500 Form?

Any organization seeking to obtain tax-exempt status in California must file the Form 3500. This includes nonprofit organizations, trusts, and limited liability companies (LLCs) that operate on a not-for-profit basis.

What documents are required to be submitted with the California 3500 Form?

Alongside the completed Form 3500, organizations need to submit:

- A copy of the organization’s creating document, such as the articles of incorporation,

- Bylaws or similar organizational documents,

- Financial statements for the current and three prior years or a proposed four-year budget for new organizations,

- And any additional information requested in specific parts of the form, such as lease agreements or lists of officers and directors.

Can foreign corporations, trusts, and LLCs apply for tax-exempt status using the California 3500 Form?

Yes, foreign corporations, trusts, and LLCs can apply for tax-exempt status in California. However, there are specific sections within the form and additional guidelines they must follow, as outlined in the form's instructions.

What happens if an organization’s tax-exempt status is not approved?

If the California Franchise Tax Board (FTB) does not approve an organization's tax-exempt status, the FTB will notify the organization detailing the reasons for denial. Organizations have the opportunity to provide additional information or clarification to address the FTB's concerns.

Is it necessary for an organization to have tax-exempt status with the IRS before applying for California tax-exempt status?

While it’s beneficial, it's not a prerequisite to have IRS tax-exempt status before applying for California tax-exempt status with Form 3500. However, organizations already recognized as tax-exempt by the IRS may qualify for a simplified process through Form 3500A, Submission of Exemption Request.

Where should the completed California 3500 Form be sent?

The completed Form 3500, along with all required attachments, should be mailed to the Exempt Organizations Unit at the following address:

- Franchise Tax Board,

- Exempt Organizations Unit MS F120,

- PO BOX 1286,

- Rancho Cordova, CA 95741-1286.

Common mistakes

Filling out the California Form 3500 can be a meticulous task, and it's common for people to make mistakes in the process. Here’s a breakdown of seven common errors to avoid:

Not providing the required organizational documents: Failing to include essential documents like the creating document of the organization can lead to delays or denial of the exemption application.

Omitting the FEIN: Forgetting to include the Federal Employer Identification Number (FEIN) can result in the inability to match the application with the organization properly.

Incorrectly answering organizational structure questions: Misunderstanding or incorrectly identifying whether the organization is a foreign corporation, a trust, or an LLC can significantly impact the application.

Skipping the narrative of activities: Providing a generic description or leaving Part II, the Narrative of Activities section, blank, rather than detailing the specific activities the organization engages in, undermines the application's validity.

Ignoring financial history: Neglecting to attach detailed income and expense statements for previously active years or a proposed budget for new organizations leaves the financial section incomplete.

Incomplete details about officers, directors, and trustees: Not listing all required information, such as names, titles, and mailing addresses for each officer, director, and trustee, or failing to mention compensation data, hampers the thorough evaluation of the organization.

Forgetting to check activities properly: Overlooking or inaccurately marking the checkboxes related to specific activities, such as fund-raising, gaming activities, or operation outside of the United States, can misrepresent the organization's functions and purpose.

Being mindful of these pitfalls and thoroughly reviewing the entire form before submission can greatly improve the chances of a successful exemption application.

Documents used along the form

Filing for tax exemption in California involves more than just completing and submitting Form 3500. To ensure a comprehensive application, organizations might need to provide additional forms and documents that give a clearer picture of their operations, structure, and financials. Understanding these adjunct requirements can significantly smooth the application process.

- Form 199 or Form 199N: These are the California Exempt Organization Annual Information Return and the California e-Postcard, respectively. Form 199 is required for most tax-exempt organizations to report their annual financial information. Smaller organizations that do not meet the threshold for filing Form 199 may file Form 199N, a simpler, electronic notice to the Franchise Tax Board (FTB).

- Articles of Incorporation: This is a document required at the start of the application process for becoming a California nonprofit. It establishes the organization’s existence and includes crucial details like the organization’s name, purpose, initial directors, and agent for service of process. Providing a copy with the Form 3500 application confirms the organization's legal structure and nonprofit status.

- Bylaws: Bylaws are another critical document for nonprofit organizations, outlining the rules that govern their operations and management. While bylaws are not filed with the California Secretary of State, they may be requested by the FTB to understand the organizational governance and operational procedures, which can impact tax-exempt status.

- IRS Determination Letter: If the organization has already obtained tax-exempt status from the Internal Revenue Service (IRS), a copy of the IRS Determination Letter should be provided. This letter is proof that the organization is recognized as tax-exempt under federal law, which can expedite the state exemption process.

These documents play a crucial role in substantiating the information provided on Form 3500 and demonstrate compliance with state and federal regulations governing nonprofits. Proper preparation and inclusion of these documents can lead to a smoother and more efficient exemption application process, ultimately allowing the organization to focus on its mission rather than bureaucratic hurdles.

Similar forms

The IRS Form 1023, Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code, shares similarities with the California Form 3500 in purpose and structure. Both forms are used by organizations seeking tax-exempt status, with Form 1023 focusing on federal exemption by the IRS and Form 3500 for state-level exemption in California. They require detailed information about the organization’s structure, activities, financial data, and governance to assess eligibility for tax-exempt status.

Form 990, Return of Organization Exempt from Income Tax, shares a commonality with parts of the California Form 3500, especially in the financial reporting section. While Form 3500 is for applying for tax-exempt status, Form 990 is an annual reporting return that certain federally tax-exempt organizations must file with the IRS. Both necessitate disclosure of financial information, including revenue and expenses, to maintain transparency and compliance with tax laws.

The California Form 199, Exempt Organization Annual Information Return, is akin to the financial data section of the California Form 3500. Form 199 is required for tax-exempt organizations in California to annually report their financial activities. Similar to part of the Form 3500 preparation process, it demands a detailed account of income, expenses, and changes in net assets to ensure the organization continues to operate within the boundaries of its exempt purposes.

Form 1024, Application for Recognition of Exemption Under Section 501(a) of the Internal Revenue Code, differs from Form 1022 in that it is used by organizations seeking tax-exempt status under codes other than 501(c)(3). Form 3500 and Form 1024 share the principle of providing comprehensive details about the organization's purpose, activities, and governance structure to prove they meet specific exemption criteria set by the respective tax authority.

Form 1041, U.S. Income Tax Return for Estates and Trusts, relates indirectly to California Form 3500 in the context of trusts declaring their activities and financial status. When trusts apply for tax-exempt status using Form 3500, they must disclose pertinent details similar to what's required on Form 1041 for taxation purposes, although the latter is focused more on annual income than exemption qualification.

The California Form 3500A, Submission of Exemption Request, is directly related to Form 3500 but serves a simpler purpose. For organizations that already have a federal exemption determination letter, Form 3500A provides a streamlined process to obtain California tax-exempt status. They both require information on organizational structure and exempt activities, but Form 3500A typically involves less documentation due to reliance on existing federal exemption recognition.

Form SS-4, Application for Employer Identification Number (EIN), though primarily for obtaining an EIN, can precede the submission of California Form 3500 as part of the organizational setup process. Accurate identification and contact information are crucial for both forms, laying the groundwork for an organization's compliance and tax-exempt filing requirements.

Form FTB 199N, California e-Postcard, is for small tax-exempt organizations in California to annually report basic information. This form and the California Form 3500 both ensure organizations meet ongoing compliance with state tax regulations, albeit at different stages and complexities of the organization's lifecycle.

The Uniform Application for Exemption, used in some jurisdictions, like the Multistate Registration and Filing Portal, parallels the California Form 3500 in its utility for non-profit registration and tax exemption on a broad level. Both forms gather detailed organizational information to evaluate and maintain tax-exempt status, emphasizing compliance with regulatory standards across different areas of operation.

Last, the Statement of Information (Form SI-100) required by the California Secretary of State for most entities, including non-profit corporations, connects with California Form 3500 in maintaining organizational compliance. While Form SI-100 updates or confirms basic entity information biennially, Form 3500 delves deeper, validating the non-profit's eligibility for state-level tax exemption initially and potentially upon renewal.

Dos and Don'ts

When filling out the California 3500 form, it is crucial to ensure that the information provided is accurate and comprehensive to avoid delays or denials in the exemption application process. Below are key dos and don’ts to consider:

- Do ensure that all information matches the organization’s creating document, including the name and address.

- Do provide clear answers to questions about the organization's structure, such as whether it is a foreign corporation, trust, or limited liability company.

- Do include a detailed narrative of the organization’s past, present, and planned activities, focusing on how these activities further the exempt purpose.

- Do attach copies of required financial documents, such as the Form 199 or FTB 199N, and provide detailed income and expense statements for the required years.

- Do list all officers, directors, and trustees accurately, including their compensation, if any.

- Don’t leave sections blank. If a question does not apply, indicate this clearly.

- Don’t forget to sign and date the form, acknowledging that the information provided is true, correct, and complete to the best of your knowledge under penalties of perjury.

Adhering to these guidelines will streamline the application process, minimizing potential obstacles that could impede the approval of the tax-exempt status.

Misconceptions

The California Form 3500, pivotal for organizations seeking tax-exempt status within the state, is often encumbered by misconceptions. A clear understanding is essential to navigate this process successfully. Below are five common misconceptions and their clarifications:

- Any organization can instantly obtain tax-exempt status with this form. In reality, the application process requires thorough documentation and adherence to specific criteria. The organization's purpose, activities, and structure are rigorously reviewed before granting exemption.

- Form 3500 is the only document needed for exemption. Contrary to this belief, organizations must provide additional information, including organizational documents, detailed narratives of activities, and financial data. Failing to provide complete and accurate information can lead to application delays or denial.

- Once exempt, always exempt. This statement is misleading. Organizations must continue to comply with legal and filing requirements, including the submission of annual information returns and maintenance of their exempt purpose. Exemption can be revoked if the organization fails to adhere to these provisions.

- LLCs cannot apply for tax exemption using Form 3500. This is incorrect. Limited Liability Companies (LLCs) can qualify for exemption if they are wholly owned by one or more recognized 501(c)(3) organizations. However, specific conditions apply, and such entities must demonstrate their operations solely advance exempt purposes.

- Foreign corporations are automatically ineligible for exemption through the California Form 3500. Although foreign corporations face additional scrutiny, they are not outright denied the possibility of exemption. They must meet specific requirements detailed in the form’s instructions and demonstrate that they primarily conduct activities benefiting the public as laid out in California’s tax exemption laws.

Disentangling these misconceptions is pivotal for organizations aspiring to achieve and maintain their tax-exempt status in California. It involves a comprehensive understanding of legal requirements and the diligent preparation of precise, detailed documentation as part of the Form 3500 application process.

Key takeaways

Understanding the California 3500 form is crucial for organizations seeking to achieve or maintain their tax-exempt status. To help streamline the application process and ensure compliance, here are six key takeaways:

- Ensure to provide all listed documents with the form to avoid delays or denial of the tax exemption request. Acceptable copies of documents are sufficient.

- Clarify the nature of the organization (e.g., foreign corporation, trust, limited liability company) as different rules and qualifications apply. Notably, LLCs must be affiliated with a nonprofit to qualify for tax-exempt status in California.

- If the organization has already secured tax-exempt status with the Internal Revenue Service, this could positively impact the application with the California Franchise Tax Board. However, it is essential to disclose this information accurately on the form.

- Comprehensive narrative of activities, including past, present, and planned activities, is required. This narrative should detail how each activity supports the organization’s exempt purpose.

- Financial data covering current and previous years, or a proposed budget for new organizations, must be submitted. This information plays a critical role in determining exemption eligibility.

- Disclose any previous or ongoing fundraising activities and specify if the organization engages in specific activities such as gaming or leasing property. Details on intellectual property rights and international operations are also required.

Completing the California 3500 form thoroughly and accurately is essential for organizations seeking exemption from state taxes. Attention to detail, coupled with ensuring all necessary documentation and information are provided, can help facilitate a smooth application process.

Different PDF Templates

Ftb Llc Fee - Information on how to correctly list your LLP's current and new information on the LLP-2 form.

Form 5805 California 2022 - It serves estates and trusts with a criterion tailored to their unique tax situations, especially concerning death and tax years.